| 【英語タイトル】China In-Vitro Diagnostics Market Size & Share Analysis - Growth Trends and Forecast (2026 - 2031)

|

| ・商品コード:MOR2884MN7745

・発行会社(調査会社):Mordor Intelligence

・発行日:2026年2月

・ページ数:120

・レポート言語:英語

・レポート形式:PDF

・納品方法:Eメール(受注後2営業日)

・調査対象地域:中国

・産業分野:医療

|

◆販売価格オプション

(消費税別)

※販売価格オプションの説明

※お支払金額:換算金額(日本円)+消費税

※納期:即日〜2営業日(3日以上かかる場合は別途表記又はご連絡)

※お支払方法:納品日+5日以内に請求書を発行・送付(請求書発行日より2ヶ月以内に銀行振込、振込先:三菱UFJ銀行/H&Iグローバルリサーチ株式会社、支払期限と方法は調整可能)

|

❖ レポートの概要 ❖

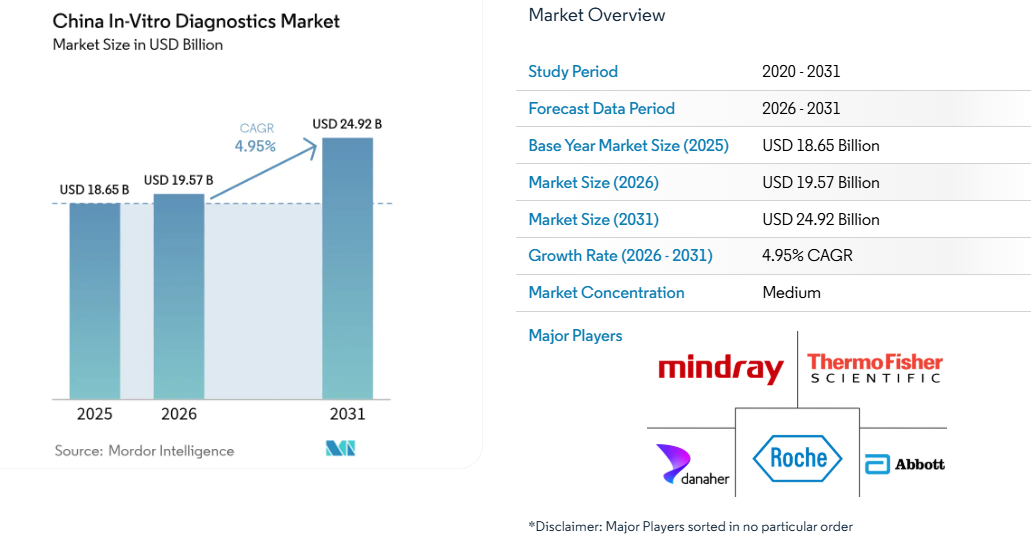

中国の体外診断薬市場規模は、2025年に186億5000万米ドル、2026年に195億7000万米ドルとなり、2031年までに249億2000万米ドルに達すると予測されており、2026年から2031年にかけて年平均成長率(CAGR)4.95%で成長すると見込まれています。

60歳以上の国民が2億9700万人、糖尿病を患う成人が1億1800万人から1億4800万人いることから、臨床需要は引き続き堅調である。しかし、数量ベースの積極的な調達改革により、各省の入札における試薬価格は最大90%まで下落した。業界再編の圧力により、多国籍企業および国内サプライヤーは、生産の現地化、品質管理システムの自動化、そして診断関連グループ(DRG)に基づく支払インセンティブに合致する、ソフトウェアを活用した高複雑度の検査への移行を余儀なくされている。同時に、2026年11月1日に発効する国家薬品監督管理局(NMPA)の改訂GMP基準により、より厳格なトレーサビリティおよび市販後監視要件が義務付けられる。これらの規制はコンプライアンスコストを増加させる一方で、競争基準も引き上げる。これらの要因が相まって、売上高の伸びは緩やかになる一方で、試薬・機器・ソフトウェアを統合したビジネスモデルへの業界の構造的転換が加速している。

慢性疾患および感染症の負担の増加

2024年には1億4,800万人の成人が糖尿病に罹患し、心血管疾患が死亡原因の40%を占めたことから、HbA1c、脂質パネル、心臓バイオマーカーに対する需要が持続的に高まっている。国立がんセンターは2024年に482万件の新規がん症例を記録し、これが腫瘍マーカーパネルや、EGFR阻害剤などの治療法に向けた次世代シーケンシング(NGS)コンパニオン診断の採用を後押しした。妊婦に対するHIV、B型肝炎、梅毒のスクリーニング検査の義務化により、免疫測定法の対象市場が拡大した。2024年8月、Daan Gene社がモンキーポックス核酸検査キットの承認を取得したことは、病原体に対する迅速な対応能力を実証するものであった。検査結果の相互承認により、重複するルーチン検査の数は減少しているものの、専門検査の実施件数は引き続き増加している。

急速な高齢化

60歳以上の層は2024年に2億9700万人に達し、2035年までに4億人に達すると予測されており、凝固検査、血液検査、腎機能検査の利用が拡大している。地域の高齢者ケアセンターでは現在、江蘇省、浙江省、四川省の1万カ所を対象とした2025年のパイロット事業の一環として、血糖値、脂質、尿酸値のモニタリングにポイント・オブ・ケア(POC)機器を導入している。Mindray社は2025年、プライマリケア向けに最適化されたコンパクトな化学発光分析装置を発売した。この装置は、WeChatを活用した検査結果の配信機能を統合しており、地方の診療所における人手不足を補うことを目的としている。規制当局による迅速審査の結果、2024年から2025年にかけて12種類の自己検査用デバイスが国家薬品監督管理局(NMPA)の承認を取得し、在宅モニタリングに対する政策的な支援が強調された。

ポイント・オブ・ケア環境への急速な分散化

「iPonatic」などのポータブルシステムは、指先からの検体を用いて30分で感染症パネル検査の結果を提供する[2]。「ポイント・オブ・ケア学」を採用した救急部門では、治療開始までの時間が大幅に短縮されたと報告されている。2,700の村診療所を対象とした農村部でのパイロット事業は、全国展開に向けた拡張可能な道筋を示している。ネットワーク接続とクラウドダッシュボードにより遠隔監視が可能となり、都市部と農村部の格差が解消されている。

分子検査およびポイント・オブ・ケア検査における技術的進歩

MGI Tech社のDNBSEQ-T20プラットフォームは、国内の次世代シーケンシング処理能力を倍増させ、2026年までに1ゲノムあたりのコストを100米ドルまで引き下げた。NMPAは2024年から2025年にかけて、BRCA1/2およびKRASアッセイを含む8つのコンパニオン診断薬を承認し、精密腫瘍学に対する公的支援を強調した。Wondfo社の15分で結果が出るトロポニンIカートリッジにより、救急部門での検査は血糖測定ストリップの枠を超えて広がった。Mindray社はDeepSeek社の大規模言語モデルを血液検査装置に組み込み、パイロット試験において手動による白血球分類を30%削減した。ソフトウェア中心の機能により、競争優位性は価格からワークフローの生産性へと再定義されつつある。

数量ベースの調達による価格下落

2024~2025年の省レベル入札により、免疫測定試薬の価格は1検査あたり15~20人民元から3~5人民元へと大幅に引き下げられ、粗利益率が30パーセントポイント低下した。これにより、ロシュとシーメンスは採算の取れないSKUから撤退した。江西省が2025年に実施した生化学試薬の入札では、平均販売価格が72%引き下げられ、中小メーカーは年間検査数100万件未満のニッチなアッセイラインの生産を中止せざるを得なくなった。31の省における検査結果の相互承認により、ルーチン検査パネルの検査数は15~20%減少した[2]。メーカー各社は、機器を原価でバンドル販売したり、入札対象外となるプレミアム検査キットに研究開発を集中させたりすることで対抗しているが、特殊なバリデーションサイクルが収益回復を遅らせている。

厳格かつ変化し続ける規制要件

2026年11月に発効するNMPAの2025年GMP改訂では、ISO 13485への準拠と原材料のトレーサビリティが義務付けられ、施設あたり2,000万~5,000万人民元のコンプライアンスコストが追加される[3]。医療機器固有識別(UDI)規則により、各メーカーはバーコードインフラに最大500万人民元の投資を必要とする。クラスIIIの承認までの期間は18~24ヶ月に延長され、製品の発売が停滞している。2024年には8社のLISベンダーに対し、合計1億2,000万人民元のデータプライバシー違反による罰金が科され、サイバーセキュリティへの投資需要が高まっている。

*当社の予測では、推進要因および抑制要因の影響を方向性として扱い、加算的なものとは見なしていない。影響予測は、ベースラインの成長、構成比の影響、および変数間の相互作用を反映している。

セグメント分析

検査種別:分子診断が主導、免疫診断が加速

2025年、分子診断は次世代シーケンシングおよび感染症パネルに支えられ、市場の38.65%を占めた。免疫診断は、地方自治体の入札において国内製の化学発光システムが輸入品に取って代わっていることから、2031年まで年平均成長率(CAGR)6.87%という最速の成長軌道に乗っている。中国の体外診断市場において、分子診断プラットフォームの市場規模はコンパニオン診断の普及に伴い拡大すると予想されるが、2025年に12種類の液体生検検査が保険適用除外となったことが、短期的な成長を抑制している。江蘇省および浙江省では、脂質検査や肝機能検査の重複を削減する相互承認政策により、臨床化学検査の検査件数が15~20%減少した。血液学分野では、ISO 15189基準に基づく旧式の3部構成分析装置の置き換えが進み、MindrayとSysmexが提供する自動スライド作成モジュールが合わせて60%のシェアを獲得した。

2025年、BGI Genomicsは500人民元の全エクソームパネルを発売し、8つの省で保険適用を獲得した。これは、シーケンシングコストの低下がアクセスの拡大につながっていることを示している。YHLOの「iFlash 3000」は、アボットの「Alinity」より45%安い価格設定で、発売初年度に700の第二級病院に導入された。分子診断が依然として最大の収益源であるものの、価格引き下げが続く中、中国の体外診断薬市場で利益率を維持するためには、ワークフローの革新と臨床的価値の実証が不可欠となっている。

製品別:試薬が主流、ソフトウェアが勢いを増す

2025年には、試薬およびキットが製品売上高の61.43%を占めたが、検査室のデジタル化に伴い、ソフトウェアおよびサービスは年平均成長率(CAGR)6.67%で成長している。DRG予算の下で機器の買い替えサイクルは長期化しているが、ベンダーは利益率ゼロの分析装置を複数年の試薬契約とセットで販売することでこれを相殺している。Mindrayの武漢複合施設はこの変化を体現しており、病院チェーン1つあたり最大10億人民元相当の消耗品契約を確保している。

国家衛生健康委員会のリアルタイムデータ提供義務化により、ミドルウェアの需要が高まっている。MindrayとアリババのAIモジュールはトロポニンの偽陽性を12%削減し、病院が再入院ペナルティを回避するのに役立っている。浙江省のブロックチェーン・リポジトリは、年間8億人民元のコスト削減効果を実証し、HL7 FHIR規格の採用を後押ししている。試薬の粗利益率が40%に圧縮される中、アフターサービス、クラウドサブスクリプション、品質管理コンサルティングは現在、大手企業の売上高の8~12%を占めており、この比率は中国の体外診断薬市場においてさらに上昇すると予想される。

用途別:使い捨て製品が主導、再利用可能機器が急増

2025年には、血糖値およびコレステロール検査のOTC承認拡大を背景に、使い捨てカートリッジ、ストリップ、マイクロ流体チップが68.65%のシェアを占めた。しかし、病院がISO 15189規格に準拠するため老朽化した分析装置を更新するにつれ、再利用可能な機器は2031年まで年平均成長率(CAGR)7.84%で成長すると予想される。中国の体外診断市場において、再利用可能な分析装置のシェアは、2015年以前に導入され、2026年に耐用年数を迎える血液検査システムの約40%に達する見込みである。

製品設計においては、接続性がますます重視されている。Mindray社の化学分析装置「BS-2000M」は、QCデータをクラウドダッシュボードにストリーミングし、校正誤差を18%低減している。Wondfo社の使い捨て15分トロポニンカートリッジは、分野間の融合を体現する好例であり、検査室レベルの感度を救急現場にもたらし、中国の体外診断薬市場におけるフォーマットの境界をさらに曖昧にしている。

用途別:感染症が最大、腫瘍学が最も急速に成長

感染症検査は、HIV、B型・C型肝炎、梅毒、結核の義務的なスクリーニングに牽引され、2025年の売上高の41.76%を占めた。腫瘍学検査は、国立がんセンターによる肺がん、大腸がん、胃がんのスクリーニングパイロット事業により、年平均成長率(CAGR)7.43%で拡大すると予測されている。糖尿病モニタリングは依然として需要の中核をなしているが、持続血糖モニタリングの普及により、検査室でのHbA1c検査件数は約9%減少した。

2024年から2025年にかけて、BRCA1/2、EGFR、KRASを網羅する8つのNMPA承認コンパニオン診断薬が、シーケンシングを腫瘍学の主流ワークフローへと押し上げている。感染症関連の検査件数は、COVID-19関連の義務化措置が終了した後に減少したが、定期的な肝炎およびHIVスクリーニングは安定している。価値に基づく医療(Value-based Care)が進展する中、高特異性の腫瘍学パネルは、中国の体外診断薬市場において巨大な利益源を獲得する立場にある。

エンドユーザー別:病院が主導、在宅医療が拡大

2025年、病院検査室は支出の52.65%を占め、自動化された血液検査および化学発光分析ラインを用いて1日最大1,000検体を処理した。病院が複雑な検査を外部委託するにつれ、独立系検査機関のシェアが拡大し、AdiconとKingMedが合わせて40%を占めた。在宅ケアおよび自己検査のユーザー数は、国家薬品監督管理局(NMPA)が承認した12種類のOTC医療機器と、民政部の高齢者ケア戦略に後押しされ、年平均成長率(CAGR)5.64%で増加する見込みである。

アンドン・ヘルスによるiHealthへの4,590万米ドルの出資は、WeChatミニプログラムに統合されたBluetooth対応の血糖値測定器および心電図測定器に対する需要の高まりを反映している。調達コストの上限に直面している病院は購買を統合しており、上位10のネットワークがすでにIVD支出の25%を占めており、中国の体外診断市場における主要顧客との取引動向が激化している。

競争環境

2025年、上位5社のサプライヤー(Mindray、Roche、Abbott、Danaher、Siemens)が市場総売上高の約30%を占めており、市場構造は適度に集中していることが示されている。国内企業は市場での地位を強化しており、Mindrayは血液検査のワークフローにAIを統合し、競争力のある価格で機器のバンドル販売を行うことで、長期的な試薬契約を確保している。同様に、YHLOは自社の化学発光システムを輸入品より45%安い価格に設定することで市場に新たな風を吹き込んだ。これに対し、多国籍企業は生産の現地化を進め、その代表例であるロシュの蘇州拠点は、国家薬品監督管理局(NMPA)の登録取得から12ヶ月以内に3億6000万元の追加売上高を生み出した。

プライベート・エクイティの活動も活発化し、アンドン・ヘルスによるiHealthへの出資や、テルゲンによる武漢ヘルスケア・バイオテックの買収が注目された。専門分野への関心も引き続き高まっており、その一例として、ベックマン・コールターが2025年11月にエーザイ・チャイナと提携し、国内の1,500万人の認知症患者を対象にアルツハイマー病のバイオマーカーを共同開発することが挙げられる。AIを活用した病理診断サービスプロバイダーのインファービジョン(Infervision)や、30分でPCR検査を完了させる革新技術を持つサンシュア・バイオテック(Sansure Biotech)といった新興のディスラプター企業は、ソフトウェア主導の差別化を活かし、中国の体外診断薬市場で競争優位性を確立しようとしている。

技術競争は、特にシーケンシングのスループットやAIを活用した解析の分野で加速している。BGI GenomicsのDNBSEQ-T20はゲノムシーケンシングのコストを100米ドルまで引き下げ、イルミナ(Illumina)の価格戦略に圧力をかけている。Mindrayとアリババクラウドが品質管理SaaSソリューションで提携したことは、業界が継続的収益モデルへと移行していることを浮き彫りにしている。さらに、大量調達イニシアチブや厳格なGMP基準への対応がM&Aを促進しており、コンプライアンスやデジタルトランスフォーメーションへの投資が可能な大規模なプレーヤーに有利に働いている。 |

The China In-Vitro Diagnostics Market size is projected to be USD 18.65 billion in 2025, USD 19.57 billion in 2026, and reach USD 24.92 billion by 2031, growing at a CAGR of 4.95% from 2026 to 2031.

With 297 million citizens aged 60 and above and 118 million to 148 million adults living with diabetes, clinical demand remains robust. However, aggressive volume-based procurement reforms have driven reagent prices in provincial tenders down by up to 90%. Consolidation pressures are compelling both multinational and domestic suppliers to localize production, automate quality systems, and transition from commodity assays to software-enabled, high-complexity testing that aligns with Diagnosis-Related Group payment incentives. Simultaneously, the National Medical Products Administration’s updated GMP standards, effective November 1, 2026, mandate stricter traceability and post-market surveillance requirements. While these regulations increase compliance costs, they also elevate competitive standards. Together, these factors moderate topline growth while accelerating the industry’s structural shift toward integrated reagent-instrument-software business models.

Rising Chronic and Infectious Disease Burden

Diabetes affected 148 million adults in 2024, and cardiovascular disease caused 40% of deaths, driving sustained demand for HbA1c, lipid panels, and cardiac biomarkers. The National Cancer Center recorded 4.82 million new cancer cases in 2024, spurring adoption of tumor-marker panels and next-generation sequencing companion diagnostics for therapies such as EGFR inhibitors. Mandatory HIV, hepatitis B, and syphilis screening for pregnant women expanded the addressable immunoassay market. Rapid pathogen response capability was demonstrated when Daan Gene secured approval for a monkeypox nucleic acid test kit in August 2024. Although mutual recognition of test results lowers duplicate routine panels, specialty assay volumes continue to rise.

Rapidly Ageing Population

The 60-plus cohort reached 297 million in 2024 and is projected to reach 400 million by 2035, escalating the use of coagulation, hematology, and renal-function assays. Community elder-care centers now deploy point-of-care devices for glucose, lipid, and uric acid monitoring under a 2025 pilot spanning 10,000 sites in Jiangsu, Zhejiang, and Sichuan. Mindray released a compact chemiluminescence analyzer in 2025, tailored for primary care, that integrates WeChat-based result delivery to offset staffing shortages in rural clinics. Regulatory fast-tracking led to NMPA clearance for 12 self-testing devices in 2024-2025, underscoring policy support for at-home monitoring.

Rapid Decentralisation to Point-of-Care Settings

Portable systems such as iPonatic deliver 30-minute infectious-disease panels from fingertip samples[2]. Emergency departments adopting “point-of-careology” report materially shorter therapeutic turnaround times. Rural pilots covering 2,700 village clinics showcase scalable pathways for nationwide deployment. Connectivity and cloud dashboards enable remote supervision, plugging urban–rural gaps.

Technological Advancements in Molecular and Point-of-Care Testing

MGI Tech’s DNBSEQ-T20 platform doubled national next-generation sequencing throughput, pushing per-genome cost to USD 100 by 2026. The NMPA cleared eight companion diagnostics between 2024-2025, including BRCA1/2 and KRAS assays, underlining official support for precision oncology. Wondfo’s 15-minute troponin-I cartridge broadened emergency-department testing beyond glucose strips. Mindray embedded DeepSeek’s large language model into hematology analyzers, reducing manual differentials by 30% in a pilot. Software-centric capabilities are redefining competitive advantage away from price toward workflow productivity.

Price Erosion from Volume-Based Procurement

Provincial tenders in 2024-2025 slashed immunoassay reagent prices to CNY 3-5 per test from CNY 15-20, wiping 30 percentage points off gross margins and prompting Roche and Siemens to exit unprofitable SKUs. Jiangxi’s 2025 biochemical-reagent round cut average selling prices by 72%, driving smaller firms to shutter niche assay lines below 1 million annual tests. Mutual recognition of results across 31 provinces trimmed routine-panel volumes 15-20%[2]. Manufacturers are countering by bundling instruments at cost and focusing R&D on premium assays that remain outside tender scope, though specialty validation cycles are delaying revenue recovery.

Stringent and Evolving Regulatory Requirements

The NMPA’s 2025 GMP revision, effective November 2026, mandates ISO 13485 alignment and raw-material traceability, adding CNY 20 million-50 million compliance costs per facility[3]. Unique device identification rules require an investment of up to CNY 5 million in each manufacturer’s barcode infrastructure. Class III approval timelines have lengthened to 18-24 months, stalling product launches. Data-privacy fines totaling CNY 120 million were levied on eight LIS vendors in 2024, intensifying cybersecurity spending needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Lead, Immunoassays Accelerate

Molecular diagnostics accounted for 38.65% of the market in 2025, underpinned by next-generation sequencing and infectious-disease panels. Immunodiagnostics is on track for the fastest 6.87% CAGR through 2031 as domestic chemiluminescence systems displace imports in provincial tenders. The China in-vitro diagnostics market size for molecular platforms is expected to rise alongside companion-diagnostic uptake, yet reimbursement exclusions for 12 liquid-biopsy assays in 2025 temper short-term growth. Clinical-chemistry volumes dropped by 15-20% in Jiangsu and Zhejiang due to mutual recognition policies that reduced duplicate lipid and liver-function tests. Hematology benefited from ISO 15189-driven replacement of legacy 3-part analyzers, with Mindray and Sysmex offering automated slide-making modules that captured 60% combined share.

In 2025, BGI Genomics launched a CNY 500 whole-exome panel and won reimbursement in eight provinces, illustrating how falling sequencing costs are broadening access. YHLO’s iFlash 3000, priced 45% below Abbott’s Alinity, penetrated 700 tier-2 hospitals within its first year. Although molecular diagnostics remains the largest revenue pool, continued price cuts necessitate workflow innovation and clinical-value demonstration to sustain margins in the China in-vitro diagnostics market.

By Product: Reagents Dominate, Software Gains Traction

Reagents and kits generated 61.43% of product revenue in 2025, yet software and services are growing at 6.67% CAGR as laboratories digitize. Instruments face lengthening replacement cycles under DRG budgets, but vendors offset this by bundling zero-margin analyzers with multi-year reagent contracts. Mindray’s Wuhan complex embodies this shift, securing consumable deals worth up to CNY 1 billion per hospital chain.

Real-time data mandates from the National Health Commission bolster middleware demand. Mindray-Alibaba AI modules cut troponin false positives by 12%, helping hospitals avoid readmission penalties. Zhejiang’s blockchain repository demonstrated CNY 800 million in annual cost savings, propelling adoption of the HL7 FHIR standard. With reagent gross margins compressed to 40%, after-sales service, cloud subscriptions, and quality-control consulting now account for 8-12% of leading firms’ sales, a ratio expected to rise within the China in-vitro diagnostics market.

By Usability: Disposables Lead, Re-Usable Equipment Surges

Disposable cartridges, strips, and microfluidic chips commanded 68.65% share in 2025, fueled by expanding OTC approvals for glucose and cholesterol tests. However, reusable equipment is expected to grow at a 7.84% CAGR through 2031 as hospitals replace aging analyzers to meet ISO 15189 standards. The China in-vitro diagnostics market share of re-usable analyzers will climb to about 40% of hematology systems installed before 2015 that hit end-of-life in 2026.

Product design increasingly emphasizes connectivity. Mindray’s BS-2000M chemistry analyzer streams QC data to cloud dashboards, lowering calibration errors by 18%. Wondfo’s disposable 15-minute troponin cartridge exemplifies cross-pollination, bringing lab-grade sensitivity to emergency settings and intensifying format blurring within the China in-vitro diagnostics market.

By Application: Infectious Diseases Largest, Oncology Fastest

Infectious-disease assays made up 41.76% of 2025 revenue, driven by mandatory HIV, hepatitis B/C, syphilis, and TB screening. Oncology tests are forecast to expand at 7.43% CAGR due to National Cancer Center screening pilots for lung, colorectal, and gastric tumors. Diabetes monitoring remains a core demand pillar, though continuous glucose monitoring has trimmed lab-based HbA1c volumes by roughly 9%.

Eight NMPA-approved companion diagnostics between 2024-2025, covering BRCA1/2, EGFR, and KRAS, are pushing sequencing into mainstream oncology workflows. Infectious-disease volumes declined after COVID-19 mandates lapsed, but routine hepatitis and HIV screening remains stable. As value-based care advances, high-specificity oncology panels are positioned to capture oversized profit pools in the China in-vitro diagnostics market.

By End User: Hospitals Dominate, Homecare Expands

Hospital laboratories absorbed 52.65% of spending in 2025, processing up to 1,000 daily samples with automated hematology and chemiluminescence lines. Stand-alone reference labs gained share as hospitals outsourced complex assays, with Adicon and KingMed holding 40% together. Home-care and self-testing users will rise at 5.64% CAGR, propelled by 12 NMPA-approved OTC devices and the Ministry of Civil Affairs’ elder-care strategy.

Andon Health’s USD 45.9 million iHealth stake taps rising demand for Bluetooth-enabled glucose and ECG devices integrated into WeChat mini-programs. Hospitals, facing procurement cost ceilings, are consolidating purchasing; the top 10 networks already represent 25% of IVD expenditure, intensifying key-account dynamics in the China in-vitro diagnostics market.

Competitive Landscape

In 2025, the top five suppliers—Mindray, Roche, Abbott, Danaher, and Siemens—accounted for approximately 30% of the market’s combined revenue, indicating a moderately concentrated market structure. Domestic players reinforced their market positions, with Mindray integrating AI into hematology workflows and offering bundled instruments at competitive prices to secure long-term reagent contracts. Similarly, YHLO disrupted the market by pricing its chemiluminescence systems 45% lower than imported alternatives. In response, multinational companies localized production, exemplified by Roche’s Suzhou hub, which generated an additional RMB 360 million in revenue within 12 months of obtaining NMPA registration.

Private equity activity intensified, highlighted by Andon Health’s investment in iHealth and Tellgen’s acquisition of Wuhan HealthCare Biotech. Specialty segments continued to attract interest, as demonstrated by Beckman Coulter’s November 2025 collaboration with Eisai China to co-develop Alzheimer’s biomarkers, targeting the country’s 15 million dementia patients. Emerging disruptors such as AI-powered pathology provider Infervision and 30-minute PCR innovator Sansure Biotech are leveraging software-driven differentiation to gain a competitive edge in China’s in vitro diagnostics market.

Technological competition is accelerating, particularly in sequencing throughput and AI-driven analytics. BGI Genomics’ DNBSEQ-T20 reduced genome sequencing costs to USD 100, pressuring Illumina’s pricing strategy. The partnership between Mindray and Alibaba Cloud on a quality-control SaaS solution highlights the industry’s shift toward recurring revenue models. Furthermore, volume-based procurement initiatives and stringent GMP upgrades are driving mergers and acquisitions, favoring large-scale players capable of funding compliance and digital transformation efforts.

1. Introduction

1.1 Study Assumptions & Market Definition

1.2 Scope Of The Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Chronic and Infectious Disease Burden

4.2.2 Rapidly Ageing Population

4.2.3 Government Healthcare Reform and Insurance Expansion

4.2.4 Technological Advancements in Molecular and Point-Of-Care Testing

4.2.5 Local Manufacturing Expansion and Import Substitution

4.2.6 Digital Health Integration and Real-Time Data Connectivity

4.3 Market Restraints

4.3.1 Price Erosion from Volume-Based Procurement

4.3.2 Stringent and Evolving Regulatory Requirements

4.3.3 Regional Disparities in Laboratory Infrastructure

4.3.4 Data Privacy and Cybersecurity Compliance Costs

4.4 Regulatory Landscape

4.5 Porter’s Five Forces

4.5.1 Threat Of New Entrants

4.5.2 Bargaining Power Of Buyers

4.5.3 Bargaining Power Of Suppliers

4.5.4 Threat Of Substitutes

4.5.5 Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

5.1 By Test Type

5.1.1 Clinical Chemistry

5.1.2 Immuno-Diagnostics

5.1.3 Molecular Diagnostics

5.1.4 Hematology

5.1.5 Coagulation

5.1.6 Microbiology

5.1.7 Other Test Types

5.2 By Product

5.2.1 Instruments

5.2.2 Reagents & Kits

5.2.3 Software & Services

5.3 By Usability

5.3.1 Disposable IVD Devices

5.3.2 Re-Usable Equipment

5.4 By Application

5.4.1 Infectious Diseases

5.4.2 Diabetes

5.4.3 Oncology

5.4.4 Cardiology

5.4.5 Auto-Immune Disorders

5.4.6 Nephrology

5.4.7 Other Applications

5.5 By End User

5.5.1 Stand-Alone Laboratories

5.5.2 Hospital-Based Laboratories

5.5.3 Point-Of-Care Settings

5.5.4 Home-Care & Self-Testing Users

6. Competitive Landscape

6.1 Market Concentration

6.2 Market Share Analysis

6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share For Key Companies, Products & Services, And Recent Developments)}

6.3.1 Abbott Laboratories

6.3.2 Agilent Technologies Inc.

6.3.3 Arkray Inc.

6.3.4 Autobio Diagnostics Co. Ltd

6.3.5 BD (Becton, Dickinson & Co.)

6.3.6 BGI Genomics Co. Ltd

6.3.7 Bio-Rad Laboratories Inc.

6.3.8 Biomérieux SA

6.3.9 Danaher Corp. (Beckman Coulter, Cepheid)

6.3.10 Daan Gene Co. Ltd

6.3.11 F. Hoffmann-La Roche AG

6.3.12 Getein Biotech Inc.

6.3.13 Maccura Biotechnology Co. Ltd

6.3.14 Sansure Biotech Inc.

6.3.15 Shanghai Kehua Bio-Engineering Co. Ltd

6.3.16 Shenzhen Mindray Bio-Medical Electronics Co. Ltd

6.3.17 Siemens Healthineers AG

6.3.18 Sysmex Corporation

6.3.19 Thermo Fisher Scientific Inc.

6.3.20 Wondfo Biotech Co. Ltd

6.3.21 Zhongshan Bio-Tech Co. Ltd

7. Market Opportunities & Future Outlook

7.1 White-Space & Unmet-Need Assessment