Chapter 1. Methodology and Scope

1.1. Market Segmentation & Scope

1.2. Segment Definitions

1.2.1. Application

1.2.2. End Use

1.2.3. Regional scope

1.2.4. Estimates and forecasts timeline

1.3. Research Methodology

1.4. Information Procurement

1.4.1. Purchased database

1.4.2. GVR’s internal database

1.4.3. Secondary sources

1.4.4. Primary research

1.4.5. Details of primary research

1.4.5.1. Data for primary interviews in North America

1.4.5.2. Data for primary interviews in Europe

1.4.5.3. Data for primary interviews in Asia Pacific

1.4.5.4. Data for primary interviews in Latin America

1.4.5.5. Data for Primary interviews in MEA

1.5. Information or Data Analysis

1.5.1. Data analysis models

1.6. Market Formulation & Validation

1.7. Model Details

1.7.1. Commodity flow analysis (Model 1)

1.7.2. Approach 1: Commodity flow approach

1.7.3. Volume price analysis (Model 2)

1.7.4. Approach 2: Volume price analysis

1.8. List of Secondary Sources

1.9. List of Primary Sources

1.10. Objectives

Chapter 2. Executive Summary

2.1. Market Outlook

2.2. Segment Outlook

2.2.1. Application outlook

2.2.2. End use outlook

2.2.3. Regional outlook

2.3. Competitive Insights

Chapter 3. Magnetoencephalography Market Variables, Trends & Scope

3.1. Market Lineage Outlook

3.1.1. Parent market outlook

3.1.2. Related/ancillary market outlook

3.2. Market Dynamics

3.2.1. Market driver analysis

3.2.1.1. Increase in prevalence of neurological disorders

3.2.1.2. Technological advancements

3.2.2. Market restraint analysis

3.2.2.1. High cost of MEG

3.2.2.2. Presence of alternative diagnostic devices

3.3. Magnetoencephalography Market Analysis Tools

3.3.1. Industry Analysis – Porter’s

3.3.1.1. Supplier power

3.3.1.2. Buyer power

3.3.1.3. Substitution threat

3.3.1.4. Threat of new entrant

3.3.1.5. Competitive rivalry

3.3.2. PESTEL Analysis

3.3.2.1. Political landscape

3.3.2.2. Technological landscape

3.3.2.3. Economic landscape

Chapter 4. Magnetoencephalography Market: Application Estimates & Trend Analysis

4.1. Segment Dashboard

4.2. Global Magnetoencephalography Application Market Movement Analysis

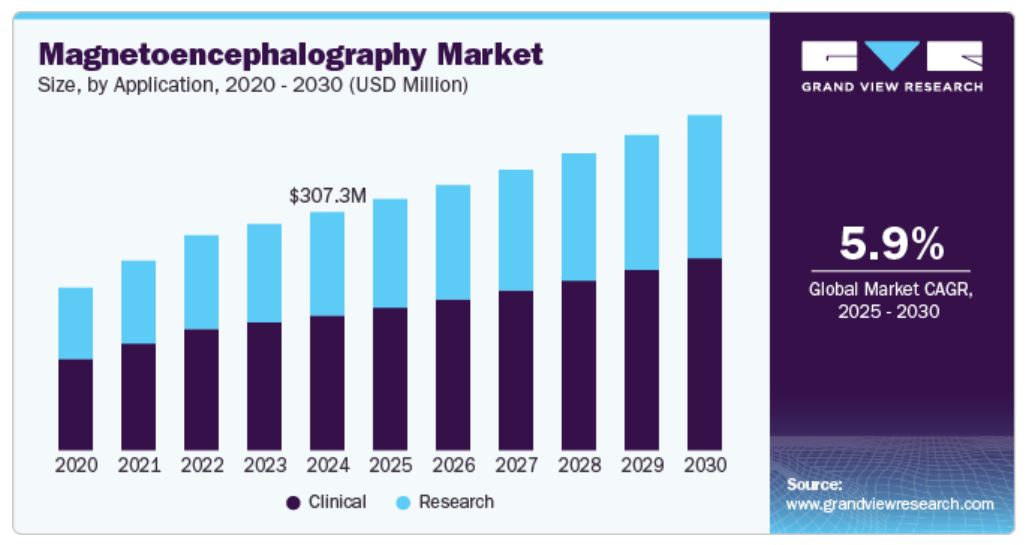

4.3. Global Magnetoencephalography Market Size & Trend Analysis, by Application, 2018 to 2030 (USD Million)

4.4. Clinical

4.4.1. Clinical market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.2. Dementia

4.4.2.1. Dementia diagnosis market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.3. Autism

4.4.3.1. Autism market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.4. Schizophrenia

4.4.4.1. Schizophrenia market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.5. Multiple Sclerosis

4.4.5.1. Multiple sclerosis market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.6. Stroke

4.4.6.1. Stroke market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.7. Epilepsy

4.4.7.1. Epilepsy market estimates and forecasts, 2018 to 2030 (USD Million)

4.4.8. Others

4.4.8.1. Others market estimates and forecasts, 2018 to 2030 (USD Million)

4.5. Research

4.5.1. Research market estimates and forecasts, 2018 to 2030 (USD Million)

Chapter 5. Magnetoencephalography Market: End Use Estimates & Trend Analysis

5.1. Segment Dashboard

5.2. Global Magnetoencephalography End Use Market Movement Analysis

5.3. Global Magnetoencephalography Market Size & Trend Analysis, by End Use, 2018 to 2030 (USD Million)

5.4. Hospitals

5.4.1. Hospitals market estimates and forecasts, 2018 to 2030 (USD Million)

5.5. Imaging Centers

5.5.1. Imaging centers market estimates and forecasts, 2018 to 2030 (USD Million)

5.6. Academic and Research Institutes

5.6.1. Academic and research institutes market estimates and forecasts, 2018 to 2030 (USD Million)

Chapter 6. Magnetoencephalography Market: Regional Estimates & Trend Analysis By Application, End Use

6.1. Regional Market Share Analysis, 2024 & 2030

6.2. Regional Market Dashboard

6.3. Global Regional Market Snapshot

6.4. Market Size, & Forecasts Trend Analysis, 2018 to 2030:

6.5. North America

6.5.1. U.S.

6.5.1.1. Key country dynamics

6.5.1.2. Competitive scenario

6.5.1.3. Regulatory framework/ reimbursement structure

6.5.1.4. U.S. market estimates and forecasts, 2018 to 2030 (USD Million)

6.5.2. Canada

6.5.2.1. Key country dynamics

6.5.2.2. Competitive scenario

6.5.2.3. Regulatory framework/ reimbursement structure

6.5.2.4. Canada market estimates and forecasts, 2018 to 2030 (USD Million)

6.5.3. Mexico

6.5.3.1. Key country dynamics

6.5.3.2. Competitive scenario

6.5.3.3. Regulatory framework/ reimbursement structure

6.5.3.4. Mexico market estimates and forecasts, 2018 to 2030 (USD Million)

6.6. Europe

6.6.1. Regulatory framework/ reimbursement structure

6.6.2. UK

6.6.2.1. Key country dynamics

6.6.2.2. Competitive scenario

6.6.2.3. Regulatory framework/ reimbursement structure

6.6.2.4. UK market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.3. Germany

6.6.3.1. Key country dynamics

6.6.3.2. Competitive scenario

6.6.3.3. Regulatory framework/ reimbursement structure

6.6.3.4. Germany market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.4. France

6.6.4.1. Key country dynamics

6.6.4.2. Competitive scenario

6.6.4.3. Regulatory framework/ reimbursement structure

6.6.4.4. France market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.5. Italy

6.6.5.1. Key country dynamics

6.6.5.2. Competitive scenario

6.6.5.3. Regulatory framework/ reimbursement structure

6.6.5.4. Italy market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.6. Spain

6.6.6.1. Key country dynamics

6.6.6.2. Competitive scenario

6.6.6.3. Regulatory framework/ reimbursement structure

6.6.6.4. Spain market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.7. Norway

6.6.7.1. Key country dynamics

6.6.7.2. Competitive scenario

6.6.7.3. Regulatory framework/ reimbursement structure

6.6.7.4. Norway market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.8. Sweden

6.6.8.1. Key country dynamics

6.6.8.2. Competitive scenario

6.6.8.3. Regulatory framework/ reimbursement structure

6.6.8.4. Sweden market estimates and forecasts, 2018 to 2030 (USD Million)

6.6.9. Denmark

6.6.9.1. Key country dynamics

6.6.9.2. Competitive scenario

6.6.9.3. Regulatory framework/ reimbursement structure

6.6.9.4. Denmark market estimates and forecasts, 2018 to 2030 (USD Million)

6.7. Asia Pacific

6.7.1. Regulatory framework/ reimbursement structure

6.7.2. Japan

6.7.2.1. Key country dynamics

6.7.2.2. Competitive scenario

6.7.2.3. Regulatory framework/ reimbursement structure

6.7.2.4. Japan market estimates and forecasts, 2018 to 2030 (USD Million)

6.7.3. China

6.7.3.1. Key country dynamics

6.7.3.2. Competitive scenario

6.7.3.3. Regulatory framework/ reimbursement structure

6.7.3.4. China market estimates and forecasts, 2018 to 2030 (USD Million)

6.7.4. India

6.7.4.1. Key country dynamics

6.7.4.2. Competitive scenario

6.7.4.3. Regulatory framework/ reimbursement structure

6.7.4.4. India market estimates and forecasts, 2018 to 2030 (USD Million)

6.7.5. Australia

6.7.5.1. Key country dynamics

6.7.5.2. Competitive scenario

6.7.5.3. Regulatory framework/ reimbursement structure

6.7.5.4. Australia market estimates and forecasts, 2018 to 2030 (USD Million)

6.7.6. South Korea

6.7.6.1. Key country dynamics

6.7.6.2. Competitive scenario

6.7.6.3. Regulatory framework/ reimbursement structure

6.7.6.4. South Korea market estimates and forecasts, 2018 to 2030 (USD Million)

6.7.7. Thailand

6.7.7.1. Key country dynamics

6.7.7.2. Competitive scenario

6.7.7.3. Regulatory framework/ reimbursement structure

6.7.7.4. Thailand market estimates and forecasts, 2018 to 2030 (USD Million)

6.8. Latin America

6.8.1. Regulatory framework/ reimbursement structure

6.8.2. Brazil

6.8.2.1. Key country dynamics

6.8.2.2. Competitive scenario

6.8.2.3. Regulatory framework/ reimbursement structure

6.8.2.4. Brazil market estimates and forecasts, 2018 to 2030 (USD Million)

6.8.3. Argentina

6.8.3.1. Key country dynamics

6.8.3.2. Competitive scenario

6.8.3.3. Regulatory framework/ reimbursement structure

6.8.3.4. Argentina market estimates and forecasts, 2018 to 2030 (USD Million)

6.9. MEA

6.9.1. Regulatory framework/ reimbursement structure

6.9.2. South Africa

6.9.2.1. Key country dynamics

6.9.2.2. Competitive scenario

6.9.2.3. Regulatory framework/ reimbursement structure

6.9.2.4. South Africa market estimates and forecasts, 2018 to 2030 (USD Million)

6.9.3. Saudi Arabia

6.9.3.1. Key country dynamics

6.9.3.2. Competitive scenario

6.9.3.3. Regulatory framework/ reimbursement structure

6.9.3.4. Saudi Arabia market estimates and forecasts, 2018 to 2030 (USD Million)

6.9.4. UAE

6.9.4.1. Key country dynamics

6.9.4.2. Competitive scenario

6.9.4.3. Regulatory framework/ reimbursement structure

6.9.4.4. UAE market estimates and forecasts, 2018 to 2030 (USD Million)

6.9.5. Kuwait

6.9.5.1. Key country dynamics

6.9.5.2. Competitive scenario

6.9.5.3. Regulatory framework/ reimbursement structure

6.9.5.4. Kuwait market estimates and forecasts, 2018 to 2030 (USD Million)

Chapter 7. Competitive Landscape

7.1. Recent Developments & Impact Analysis, By Key Market Participants

7.2. Company/Competition Categorization

7.3. Key company market share analysis, 2024

7.4. Company Position Analysis

7.5. Company Categorization (Emerging Players, Innovators and Leaders

7.6. Company Profiles

7.6.1. Compumedics Limited

7.6.1.1. Company overview

7.6.1.2. Financial performance

7.6.1.3. Product benchmarking

7.6.1.4. Strategic initiatives

7.6.2. MEGIN

7.6.2.1. Company overview

7.6.2.2. Financial performance

7.6.2.3. Product benchmarking

7.6.2.4. Strategic initiatives

7.6.3. Ricoh

7.6.3.1. Company overview

7.6.3.2. Financial performance

7.6.3.3. Product benchmarking

7.6.3.4. Strategic initiatives

7.6.4. CTF MEG NEURO INNOVATIONS, INC.

7.6.4.1. Company overview

7.6.4.2. Financial performance

7.6.4.3. Product benchmarking

7.6.4.4. Strategic initiatives

7.6.5. FieldLine Inc.

7.6.5.1. Company overview

7.6.5.2. Financial performance

7.6.5.3. Product benchmarking

7.6.5.4. Strategic initiatives

7.6.6. Cerca Magnetics Limited

7.6.6.1. Company overview

7.6.6.2. Financial performance

7.6.6.3. Product benchmarking

7.6.6.4. Strategic initiatives

List of Tables

Table 1 List of secondary sources

Table 2 List of abbreviations

Table 3 Global magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 4 Global magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 5 North America magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 6 North America magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 7 North America magnetoencephalography market by Country, 2018 – 2030 (USD Million)

Table 8 U.S. magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 9 U.S. magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 10 Canada magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 11 Canada magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 12 Mexico magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 13 Mexico magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 14 Europe magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 15 Europe magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 16 Europe magnetoencephalography market by Country, 2018 – 2030 (USD Million)

Table 17 UK magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 18 UK magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 19 Germany magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 20 Germany magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 21 France magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 22 France magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 23 Italy magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 24 Italy magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 25 Spain magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 26 Spain magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 27 Denmark magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 28 Denmark magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 29 Sweden magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 30 Sweden magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 31 Norway magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 32 Norway magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 33 Asia Pacific magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 34 Asia Pacific magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 35 Asia Pacific magnetoencephalography market by Country, 2018 – 2030 (USD Million)

Table 36 China magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 37 China magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 38 Japan magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 39 Japan magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 40 India magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 41 India magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 42 Australia magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 43 Australia magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 44 Thailand magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 45 Thailand magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 46 South Korea magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 47 South Korea magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 48 Latin America magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 49 Latin America magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 50 Latin America magnetoencephalography market by Country, 2018 – 2030 (USD Million)

Table 51 Brazil magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 52 Brazil magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 53 Argentina magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 54 Argentina magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 55 Middle East & Africa magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 56 Middle East & Africa magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 57 Middle East & Africa magnetoencephalography market by Country, 2018 – 2030 (USD Million)

Table 58 South Africa magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 59 South Africa magnetoencephalography market by Product, 2018 – 2030 (USD Million)

Table 60 South Africa magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 61 Saudi Arabia magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 62 Saudi Arabia magnetoencephalography market by Product, 2018 – 2030 (USD Million)

Table 63 Saudi Arabia magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 64 UAE magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 65 UAE magnetoencephalography market by Product, 2018 – 2030 (USD Million)

Table 66 UAE magnetoencephalography market by End Use, 2018 – 2030 (USD Million)

Table 67 Kuwait magnetoencephalography market by Application, 2018 – 2030 (USD Million)

Table 68 Kuwait magnetoencephalography market by Product, 2018 – 2030 (USD Million)

Table 69 Kuwait magnetoencephalography market by End Use, 2018 – 2030 (USD Million)