| 【英語タイトル】Japan Digital Health Market Report by Type (Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, and Others), Component (Software, Hardware, Service), and Region 2025-2033

|

| ・商品コード:IMA3008AS334

・発行会社(調査会社):IMARC

・発行日:2025年4月

・ページ数:約120

・レポート言語:英語

・レポート形式:PDF

・納品方法:Eメール(受注後2-3営業日)

・調査対象地域:グローバル

・産業分野:IT、医療

|

◆販売価格オプション

(消費税別)

※販売価格オプションの説明

※お支払金額:換算金額(日本円)+消費税

※納期:即日〜2営業日(3日以上かかる場合は別途表記又はご連絡)

※お支払方法:納品日+5日以内に請求書を発行・送付(請求書発行日より2ヶ月以内に銀行振込、振込先:三菱UFJ銀行/H&Iグローバルリサーチ株式会社、支払期限と方法は調整可能)

|

❖ レポートの概要 ❖

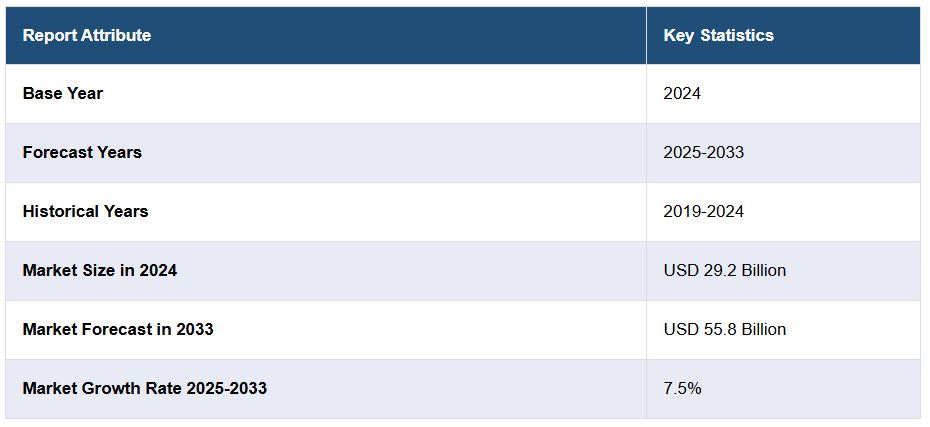

2024年、日本のデジタルヘルス市場規模は約292億ドルに達し、IMARC Groupの予測によれば、2033年には約558億ドルに拡大するとされ、2025年から2033年にかけての年平均成長率(CAGR)は7.5%に達すると見込まれています。この成長の背景には、糖尿病や心疾患などの慢性疾患の増加、医療分野における技術革新、そしてCOVID-19パンデミックの影響などが挙げられます。

デジタルヘルスとは、医療サービスの質やアクセス性を向上させるために、デジタル技術とデータを活用する分野であり、主に遠隔医療、電子カルテ(EHR/EMR)、ウェアラブルデバイス、モバイル医療アプリなどを含みます。これにより、患者は場所に関係なく個別化された医療を受けやすくなり、医師もリアルタイムで診断・治療・モニタリングを行うことが可能になります。また、患者と医療従事者間の情報共有やコミュニケーションが容易になり、より包括的かつ効率的な医療判断が可能となります。

市場成長を促す主な要因としては、慢性疾患の拡大に加え、AI、ビッグデータ、IoTなどの技術進展が医療の質と効率を高めていることが挙げられます。政府も、医療の相互運用性や標準化を進める法整備を行い、技術導入を後押ししています。加えて、医療費の高騰への対策として、デジタルヘルスがコスト効率の良い選択肢として注目されています。COVID-19を契機に、遠隔診療や在宅モニタリングの需要が一気に高まり、市場の普及が加速しました。

さらに、消費者側でも個別化された医療や利便性の高いサービスへの関心が高まり、患者自身が健康データや治療方針をより主体的に管理したいというニーズが強まっています。こうした動きを背景に、テクノロジー企業と医療機関との連携も活発化しており、より洗練されたデジタルヘルスソリューションの開発が進んでいます。

市場は「タイプ」と「構成要素」の2軸で分類されており、タイプ別では遠隔医療、医療用ウェアラブル、電子カルテ、医療アプリ、ヘルスケアアナリティクスなどに分類されます。構成要素別では、ソフトウェア、ハードウェア、サービスの3つに分かれており、それぞれの分野で成長が見込まれています。今後も医療のデジタル化と患者中心の医療への移行が進む中で、デジタルヘルス市場は日本においても重要性を増すと予想されます。 |

The Japan digital health market size reached USD 29.2 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 55.8 Billion by 2033, exhibiting a growth rate (CAGR) of 7.5% during 2025-2033. The prevalence of chronic diseases, such as diabetes and heart disorders, ongoing technological advancements across the healthcare industry, and the outbreak of the COVID-19 pandemic across the country represent some of the key factors driving the market.

Digital health refers to the use of digital technologies and data to enhance healthcare delivery and personal wellness. It encompasses various subfields, such as telemedicine, electronic health records, wearable devices, and mobile health applications. Digital health aims to provide more personalized care, making healthcare more efficient and accessible to patients, regardless of their location. The integration of technology in healthcare also enables medical professionals to monitor, diagnose, and treat patients in real time, which can improve outcomes and reduce costs. Furthermore, digital health promotes collaboration between patients and healthcare providers by facilitating communication and information sharing. This allows for a more holistic view of a patient’s health and enables more informed decision-making. The trend towards digital health reflects a broader shift in healthcare, emphasizing prevention and patient-centric care, supported by data-driven insights. Digital health is revolutionizing the way healthcare is delivered, promoting better patient engagement, improving accessibility, and offering tools that empower both patients and healthcare providers to manage health more effectively. It’s an essential component of modern healthcare, aligning technology and healthcare practices for the betterment of patient care.

Japan Digital Health Market Trends:

Digital health, a rapidly growing sector, is propelled by the increasing global prevalence of chronic diseases, such as diabetes and heart disorders. This necessitates a more streamlined approach to healthcare management; one that digital health can efficiently provide. Simultaneously, ongoing technological advancements, such as AI, big data analytics, and telemedicine, are creating opportunities to enhance patient care, diagnosis, and treatment. Along with this, governments and regulatory bodies are also supporting digital health by enforcing laws and regulations that foster integration and interoperability, reflecting a societal move towards embracing technology in healthcare. In addition, the rise in healthcare costs is pushing the need for cost-effective solutions, and digital health tools can offer affordability without compromising quality. Apart from this, the COVID-19 pandemic has additionally accelerated the adoption of digital health platforms, emphasizing the need for remote patient monitoring and virtual consultations. In confluence with this, consumer demand for personalized and convenient healthcare is also on the rise, with patients seeking more control over their health data and treatment plans. Furthermore, partnerships and collaborations between tech companies and healthcare providers are paving the way for more comprehensive and tailored digital health solutions. Some of the other factors driving the market include the growing penetration of the Internet of Things (IoT), rapid digitization, and inflating disposable income levels of individuals.

Japan Digital Health Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Japan digital health market report, along with forecasts at the country level for 2025-2033. Our report has categorized the market based on type and component.

Type Insights:

Telehealth

Medical Wearables

EMR/EHR Systems

Medical Apps

Healthcare Analytics

Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes telehealth, medical wearables, EMR/EHR systems, medical apps, healthcare analytics, and others.

Component Insights:

Software

Hardware

Service

1 Preface

2 Scope and Methodology

2.1 Objectives of the Study

2.2 Stakeholders

2.3 Data Sources

2.3.1 Primary Sources

2.3.2 Secondary Sources

2.4 Market Estimation

2.4.1 Bottom-Up Approach

2.4.2 Top-Down Approach

2.5 Forecasting Methodology

3 Executive Summary

4 Japan Digital Health Market – Introduction

4.1 Overview

4.2 Market Dynamics

4.3 Industry Trends

4.4 Competitive Intelligence

5 Japan Digital Health Market Landscape

5.1 Historical and Current Market Trends (2019-2024)

5.2 Market Forecast (2025-2033)

6 Japan Digital Health Market – Breakup by Type

6.1 Telehealth

6.1.1 Overview

6.1.2 Historical and Current Market Trends (2019-2024)

6.1.3 Market Forecast (2025-2033)

6.2 Medical Wearables

6.2.1 Overview

6.2.2 Historical and Current Market Trends (2019-2024)

6.2.3 Market Forecast (2025-2033)

6.3 EMR/EHR Systems

6.3.1 Overview

6.3.2 Historical and Current Market Trends (2019-2024)

6.3.3 Market Forecast (2025-2033)

6.4 Medical Apps

6.4.1 Overview

6.4.2 Historical and Current Market Trends (2019-2024)

6.4.3 Market Forecast (2025-2033)

6.5 Healthcare Analytics

6.5.1 Overview

6.5.2 Historical and Current Market Trends (2019-2024)

6.5.3 Market Forecast (2025-2033)

6.6 Others

6.6.1 Historical and Current Market Trends (2019-2024)

6.6.2 Market Forecast (2025-2033)

7 Japan Digital Health Market – Breakup by Component

7.1 Software

7.1.1 Overview

7.1.2 Historical and Current Market Trends (2019-2024)

7.1.3 Market Forecast (2025-2033)

7.2 Hardware

7.2.1 Overview

7.2.2 Historical and Current Market Trends (2019-2024)

7.2.3 Market Forecast (2025-2033)

7.3 Service

7.3.1 Overview

7.3.2 Historical and Current Market Trends (2019-2024)

7.3.3 Market Forecast (2025-2033)

8 Japan Digital Health Market – Breakup by Region

8.1 Kanto Region

8.1.1 Overview

8.1.2 Historical and Current Market Trends (2019-2024)

8.1.3 Market Breakup by Type

8.1.4 Market Breakup by Component

8.1.5 Key Players

8.1.6 Market Forecast (2025-2033)

8.2 Kinki Region

8.2.1 Overview

8.2.2 Historical and Current Market Trends (2019-2024)

8.2.3 Market Breakup by Type

8.2.4 Market Breakup by Component

8.2.5 Key Players

8.2.6 Market Forecast (2025-2033)

8.3 Central/ Chubu Region

8.3.1 Overview

8.3.2 Historical and Current Market Trends (2019-2024)

8.3.3 Market Breakup by Type

8.3.4 Market Breakup by Component

8.3.5 Key Players

8.3.6 Market Forecast (2025-2033)

8.4 Kyushu-Okinawa Region

8.4.1 Overview

8.4.2 Historical and Current Market Trends (2019-2024)

8.4.3 Market Breakup by Type

8.4.4 Market Breakup by Component

8.4.5 Key Players

8.4.6 Market Forecast (2025-2033)

8.5 Tohoku Region

8.5.1 Overview

8.5.2 Historical and Current Market Trends (2019-2024)

8.5.3 Market Breakup by Type

8.5.4 Market Breakup by Component

8.5.5 Key Players

8.5.6 Market Forecast (2025-2033)

8.6 Chugoku Region

8.6.1 Overview

8.6.2 Historical and Current Market Trends (2019-2024)

8.6.3 Market Breakup by Type

8.6.4 Market Breakup by Component

8.6.5 Key Players

8.6.6 Market Forecast (2025-2033)

8.7 Hokkaido Region

8.7.1 Overview

8.7.2 Historical and Current Market Trends (2019-2024)

8.7.3 Market Breakup by Type

8.7.4 Market Breakup by Component

8.7.5 Key Players

8.7.6 Market Forecast (2025-2033)

8.8 Shikoku Region

8.8.1 Overview

8.8.2 Historical and Current Market Trends (2019-2024)

8.8.3 Market Breakup by Type

8.8.4 Market Breakup by Component

8.8.5 Key Players

8.8.6 Market Forecast (2025-2033)

9 Japan Digital Health Market – Competitive Landscape

9.1 Overview

9.2 Market Structure

9.3 Market Player Positioning

9.4 Top Winning Strategies

9.5 Competitive Dashboard

9.6 Company Evaluation Quadrant

10 Profiles of Key Players

10.1 Company A

10.1.1 Business Overview

10.1.2 Services Offered

10.1.3 Business Strategies

10.1.4 SWOT Analysis

10.1.5 Major News and Events

10.2 Company B

10.2.1 Business Overview

10.2.2 Services Offered

10.2.3 Business Strategies

10.2.4 SWOT Analysis

10.2.5 Major News and Events

10.3 Company C

10.3.1 Business Overview

10.3.2 Services Offered

10.3.3 Business Strategies

10.3.4 SWOT Analysis

10.3.5 Major News and Events

10.4 Company D

10.4.1 Business Overview

10.4.2 Services Offered

10.4.3 Business Strategies

10.4.4 SWOT Analysis

10.4.5 Major News and Events

10.5 Company E

10.5.1 Business Overview

10.5.2 Services Offered

10.5.3 Business Strategies

10.5.4 SWOT Analysis

10.5.5 Major News and Events

Company names have not been provided here as this is a sample TOC. Complete list to be provided in the final report.

11 Japan Digital Health Market – Industry Analysis

11.1 Drivers, Restraints, and Opportunities

11.1.1 Overview

11.1.2 Drivers

11.1.3 Restraints

11.1.4 Opportunities

11.2 Porters Five Forces Analysis

11.2.1 Overview

11.2.2 Bargaining Power of Buyers

11.2.3 Bargaining Power of Suppliers

11.2.4 Degree of Competition

11.2.5 Threat of New Entrants

11.2.6 Threat of Substitutes

11.3 Value Chain Analysis

12 Appendix