Chapter 1. Methodology and Scope

1.1. Market Segmentation and Scope

1.2. Market Definitions

1.2.1. Product

1.2.2. Application

1.2.3. Type

1.2.4. End Use

1.3. Information analysis

1.4. Market formulation & data visualization

1.5. Data validation & publishing

1.6. Information Procurement

1.6.1. Primary Research

1.7. Information or Data Analysis

1.8. Market Formulation & Validation

1.9. Market Model

1.10. Objectives

Chapter 2. Executive Summary

2.1. Market Snapshot

2.2. Segment Snapshot

2.3. Competitive Landscape Snapshot

Chapter 3. Market Variables, Trends, & Scope

3.1. Market Lineage Outlook

3.1.1. Parent Market Outlook

3.1.2. Ancillary Market Outlook

3.2. Market Trends and Outlook

3.3. Market Dynamics

3.3.1. Market Driver Impact Analysis

3.3.1.1. Expansion of biosimilars and biologics

3.3.1.2. Growth in stem cell research

3.3.1.3. Emerging cell culture technologies for cell-based vaccines

3.3.2. Market Restraint Impact Analysis

3.3.2.1. Ethical issues concerning the use of animal-derived products

3.3.2.2. Stringent regulatory guidelines

3.4. Business Environment Analysis

3.4.1. PESTLE Analysis

3.4.2. PORTER’S Five Forces Analysis

3.4.3. COVID-19 Impact Analysis

Chapter 4. Product Business Analysis

4.1. Product Segment Dashboard

4.2. Global Cell Culture Media Market Product, Movement Analysis

4.3. Global Cell Culture Media Market Size & Trend Analysis, by Product, 2018 to 2030 (USD Million)

4.4. Serum-free Media

4.4.1. Global serum-free media market estimates and forecasts, 2018 – 2030 (USD Million)

4.4.2. CHO Media

4.4.2.1. Global CHO media market estimates and forecasts, 2018 – 2030 (USD Million)

4.4.3. HEK 293 media

4.4.3.1. Global HEK 293 media market estimates and forecasts, 2018 – 2030 (USD Million)

4.4.4. BHK media

4.4.4.1. Global BHK media market estimates and forecasts, 2018 – 2030 (USD Million)

4.4.5. Vero medium

4.4.5.1. Global vero medium market estimates and forecasts, 2018 – 2030 (USD Million)

4.4.6. Other serum-free media

4.4.6.1. Global other serum-free media market estimates and forecasts, 2018 – 2030 (USD Million)

4.5. Classical Media

4.5.1. Global classical media market estimates and forecasts, 2018 – 2030 (USD Million)

4.6. Stem Cell Culture Media

4.6.1. Global stem cell culture media market estimates and forecasts, 2018 – 2030 (USD Million)

4.7. Chemically Defined Media

4.7.1. Global chemically defined media market estimates and forecasts, 2018 – 2030 (USD Million)

4.8. Specialty Media

4.8.1. Global speciality media market estimates and forecasts, 2018 – 2030 (USD Million)

4.9. Other Cell Culture Media

4.9.1. Global other cell culture media market estimates and forecasts, 2018 – 2030 (USD Million)

Chapter 5. Type Business Analysis

5.1. Type Segment Dashboard

5.2. Global Cell Culture Media Market Type, Movement Analysis

5.3. Global Cell Culture Media Market Size & Trend Analysis, by Type, 2018 to 2030 (USD Million)

5.4. Liquid Media

5.4.1. Global liquid media market estimates and forecasts, 2018 – 2030 (USD Million)

5.5. Semisolid & Solid Media

5.5.1. Global semi-solid & solid media market estimates and forecasts, 2018 – 2030 (USD Million)

Chapter 6. Application Business Analysis

6.1. Application Segment Dashboard

6.2. Global Cell Culture Media Market Application, Movement Analysis

6.3. Global Cell Culture Media Market Size & Trend Analysis, by Application, 2018 to 2030 (USD Million)

6.4. Biopharmaceutical Production

6.4.1. Global biopharmaceutical production market estimates and forecasts, 2018 – 2030 (USD Million)

6.4.2. Monoclonal antibodies

6.4.2.1. Global monoclonal antibodies market estimates and forecasts, 2018 – 2030 (USD Million)

6.4.3. Vaccines production

6.4.3.1. Global vaccines production market estimates and forecasts, 2018 – 2030 (USD Million)

6.4.4. Other therapeutic proteins

6.4.4.1. Global other therapeutic proteins market estimates and forecasts, 2018 – 2030 (USD Million)

6.5. Diagnostics

6.5.1. Global diagnostics market estimates and forecasts, 2018 – 2030 (USD Million)

6.6. Drug Screening & Development

6.6.1. Global drug screening & development market estimates and forecasts, 2018 – 2030 (USD Million)

6.7. Tissue Engineering & Regenerative Medicine

6.7.1. Global tissue engineering & regenerative medicine market estimates and forecasts, 2018 – 2030 (USD Million)

6.7.2. Cell & gene therapy

6.7.2.1. Global cell & gene therapy market estimates and forecasts, 2018 – 2030 (USD Million)

6.7.3. Other tissue engineering & regenerative medicine

6.7.3.1. Global other tissue engineering & regenerative medicine market estimates and forecasts, 2018 – 2030 (USD Million)

6.8. Other Applications

6.8.1. Global other applications market estimates and forecasts, 2018 – 2030 (USD Million)

Chapter 7. End Use Business Analysis

7.1. End Use Segment Dashboard

7.2. Global Cell Culture Media Market End Use, Movement Analysis

7.3. Global Cell Culture Media Market Size & Trend Analysis, by End Use, 2018 to 2030 (USD Million)

7.4. Pharmaceutical & Biotechnology Companies

7.4.1. Global pharmaceutical & biotechnology companies market estimates and forecasts, 2018 – 2030 (USD Million)

7.5. Hospitals & Diagnostic Laboratories

7.5.1. Global hospitals & diagnostic laboratories market estimates and forecasts, 2018 – 2030 (USD Million)

7.6. Research & Academic Institutes

7.6.1. Global research & academic institutes market estimates and forecasts, 2018 – 2030 (USD Million)

7.7. Other End Use

7.7.1. Global other end user market estimates and forecasts, 2018 – 2030 (USD Million)

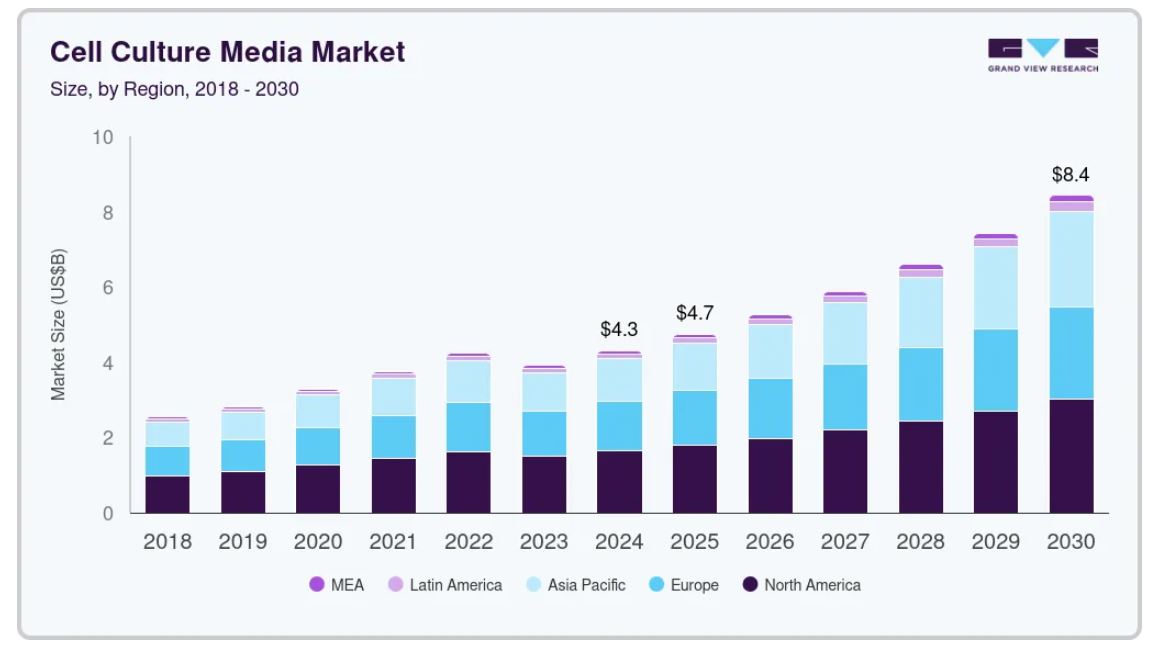

Chapter 8. Cell Culture Media Market: Regional Estimates and Trend Analysis, by Product, Type, Application, & End-Use

8.1. Regional Dashboard

8.2. Market Size & Forecasts and Trend Analysis, 2018 to 2030

8.3. North America

8.3.1. North America cell culture media market, 2018 – 2030 (USD Million)

8.3.2. U.S.

8.3.2.1. Key Country Dynamics

8.3.2.2. Competitive Scenario

8.3.2.3. Regulatory Framework

8.3.2.4. U.S. cell culture media market, 2018 – 2030 (USD Million)

8.3.3. Canada

8.3.3.1. Key Country Dynamics

8.3.3.2. Competitive Scenario

8.3.3.3. Regulatory Framework

8.3.3.4. Canada cell culture media market, 2018 – 2030 (USD Million)

8.3.4. Mexico

8.3.4.1. Key Country Dynamics

8.3.4.2. Competitive Scenario

8.3.4.3. Regulatory Framework

8.3.4.4. Mexcio cell culture media market, 2018 – 2030 (USD Million)

8.4. Europe

8.4.1. Europe cell culture media market, 2018 – 2030 (USD Million)

8.4.2. UK

8.4.2.1. Key Country Dynamics

8.4.2.2. Competitive Scenario

8.4.2.3. Regulatory Framework

8.4.2.4. UK cell culture media market, 2018 – 2030 (USD Million)

8.4.3. Germany

8.4.3.1. Key Country Dynamics

8.4.3.2. Competitive Scenario

8.4.3.3. Regulatory Framework

8.4.3.4. Germany cell culture media market, 2018 – 2030 (USD Million)

8.4.4. France

8.4.4.1. Key Country Dynamics

8.4.4.2. Competitive Scenario

8.4.4.3. Regulatory Framework

8.4.4.4. France cell culture media market, 2018 – 2030 (USD Million)

8.4.5. Italy

8.4.5.1. Key Country Dynamics

8.4.5.2. Competitive Scenario

8.4.5.3. Regulatory Framework

8.4.5.4. Italy cell culture media market, 2018 – 2030 (USD Million)

8.4.6. Spain

8.4.6.1. Key Country Dynamics

8.4.6.2. Competitive Scenario

8.4.6.3. Regulatory Framework

8.4.6.4. Spain cell culture media market, 2018 – 2030 (USD Million)

8.4.7. Denmark

8.4.7.1. Key Country Dynamics

8.4.7.2. Competitive Scenario

8.4.7.3. Regulatory Framework

8.4.7.4. Denmark cell culture media market, 2018 – 2030 (USD Million)

8.4.8. Sweden

8.4.8.1. Key Country Dynamics

8.4.8.2. Competitive Scenario

8.4.8.3. Regulatory Framework

8.4.8.4. Sweden cell culture media market, 2018 – 2030 (USD Million)

8.4.9. Norway

8.4.9.1. Key Country Dynamics

8.4.9.2. Competitive Scenario

8.4.9.3. Regulatory Framework

8.4.9.4. Norway cell culture media market, 2018 – 2030 (USD Million)

8.5. Asia Pacific

8.5.1. Asia Pacific cell culture media market, 2018 – 2030 (USD Million)

8.5.2. Japan

8.5.2.1. Key Country Dynamics

8.5.2.2. Competitive Scenario

8.5.2.3. Regulatory Framework

8.5.2.4. Japan cell culture media market, 2018 – 2030 (USD Million)

8.5.3. China

8.5.3.1. Key Country Dynamics

8.5.3.2. Competitive Scenario

8.5.3.3. Regulatory Framework

8.5.3.4. China cell culture media market, 2018 – 2030 (USD Million)

8.5.4. India

8.5.4.1. Key Country Dynamics

8.5.4.2. Competitive Scenario

8.5.4.3. Regulatory Framework

8.5.4.4. India cell culture media market, 2018 – 2030 (USD Million)

8.5.5. Singapore

8.5.5.1. Key Country Dynamics

8.5.5.2. Competitive Scenario

8.5.5.3. Regulatory Framework

8.5.5.4. Singapore cell culture media market, 2018 – 2030 (USD Million)

8.5.6. Australia

8.5.6.1. Key Country Dynamics

8.5.6.2. Competitive Scenario

8.5.6.3. Regulatory Framework

8.5.6.4. Australia cell culture media market, 2018 – 2030 (USD Million)

8.5.7. Thailand

8.5.7.1. Key Country Dynamics

8.5.7.2. Competitive Scenario

8.5.7.3. Regulatory Framework

8.5.7.4. Thailand cell culture media market, 2018 – 2030 (USD Million)

8.5.8. South Korea

8.5.8.1. Key Country Dynamics

8.5.8.2. Competitive Scenario

8.5.8.3. Regulatory Framework

8.5.8.4. South Korea cell culture media market, 2018 – 2030 (USD Million)

8.6. Latin America

8.6.1. Latin America cell culture media market, 2018 – 2030 (USD Million)

8.6.2. Brazil

8.6.2.1. Key Country Dynamics

8.6.2.2. Competitive Scenario

8.6.2.3. Regulatory Framework

8.6.2.4. Brazil cell culture media market, 2018 – 2030 (USD Million)

8.6.3. Argentina

8.6.3.1. Key Country Dynamics

8.6.3.2. Competitive Scenario

8.6.3.3. Regulatory Framework

8.6.3.4. Argentina cell culture media market, 2018 – 2030 (USD Million)

8.7. MEA

8.7.1. MEA cell culture media market, 2018 – 2030 (USD Million)

8.7.2. South Africa

8.7.2.1. Key Country Dynamics

8.7.2.2. Competitive Scenario

8.7.2.3. Regulatory Framework

8.7.2.4. South Africa cell culture media market, 2018 – 2030 (USD Million)

8.7.3. Saudi Arabia

8.7.3.1. Key Country Dynamics

8.7.3.2. Competitive Scenario

8.7.3.3. Regulatory Framework

8.7.3.4. Saudi Arabia cell culture media market, 2018 – 2030 (USD Million)

8.7.4. UAE

8.7.4.1. Key Country Dynamics

8.7.4.2. Competitive Scenario

8.7.4.3. Regulatory Framework

8.7.4.4. UAE cell culture media market, 2018 – 2030 (USD Million)

8.7.5. Kuwait

8.7.5.1. Key Country Dynamics

8.7.5.2. Competitive Scenario

8.7.5.3. Regulatory Framework

8.7.5.4. Kuwait cell culture media market, 2018 – 2030 (USD Million)

Chapter 9. Competitive Landscape

9.1. Company Categorization

9.2. Strategy Mapping

9.3. Company Market Position Analysis, 2024

9.4. Company Profiles/Listing

9.4.1. Sartorius AG

9.4.1.1. Overview

9.4.1.2. Financial Performance

9.4.1.3. Product Benchmarking

9.4.1.4. Strategic Initiatives

9.4.2. Danaher

9.4.2.1. Overview

9.4.2.2. Financial Performance

9.4.2.3. Product Benchmarking

9.4.2.4. Strategic Initiatives

9.4.3. Merck KGaA

9.4.3.1. Overview

9.4.3.2. Financial Performance

9.4.3.3. Product Benchmarking

9.4.3.4. Strategic Initiatives

9.4.4. Thermo Fisher Scientific, Inc.

9.4.4.1. Overview

9.4.4.2. Financial Performance

9.4.4.3. Product Benchmarking

9.4.4.4. Strategic Initiatives

9.4.5. FUJIFILM Corporation

9.4.5.1. Overview

9.4.5.2. Financial Performance

9.4.5.3. Product Benchmarking

9.4.5.4. Strategic Initiatives

9.4.6. Lonza

9.4.6.1. Overview

9.4.6.2. Financial Performance

9.4.6.3. Product Benchmarking

9.4.6.4. Strategic Initiatives

9.4.7. BD

9.4.7.1. Overview

9.4.7.2. Financial Performance

9.4.7.3. Product Benchmarking

9.4.7.4. Strategic Initiatives

9.4.8. STEMCELL Technologies

9.4.8.1. Overview

9.4.8.2. Financial Performance

9.4.8.3. Product Benchmarking

9.4.8.4. Strategic Initiatives

9.4.9. Cell Biologics, Inc.

9.4.9.1. Overview

9.4.9.2. Financial Performance

9.4.9.3. Product Benchmarking

9.4.9.4. Strategic Initiatives

9.4.10. PromoCell GmbH

9.4.10.1. Overview

9.4.10.2. Financial Performance

9.4.10.3. Product Benchmarking

9.4.10.4. Strategic Initiatives

List of Tables

Table 1. List of Secondary Sources

Table 2. List of Abbreviations

Table 3. Global Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 4. Global Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 5. Global Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 6. Global Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 7. Global Cell Culture Media Market, by Region, 2018 – 2030 (USD Million)

Table 8. North America Cell Culture Media Market, by Country, 2018 – 2030 (USD Million)

Table 9. North America Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 10. North America Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 11. North America Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 12. North America Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 13. U.S. Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 14. U.S. Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 15. U.S. Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 16. U.S. Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 17. Canada Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 18. Canada Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 19. Canada Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 20. Canada Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 21. Mexico Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 22. Mexico Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 23. Mexico Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 24. Mexico Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 25. Europe Cell Culture Media Market, by Country, 2018 – 2030 (USD Million)

Table 26. Europe Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 27. Europe Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 28. Europe Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 29. Europe Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 30. Germany Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 31. Germany Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 32. Germany Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 33. Germany Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 34. UK Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 35. UK Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 36. UK Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 37. UK Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 38. France Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 39. France Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 40. France Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 41. France Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 42. Italy Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 43. Italy Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 44. Italy Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 45. Italy Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 46. Spain Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 47. Spain Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 48. Spain Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 49. Spain Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 50. Denmark Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 51. Denmark Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 52. Denmark Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 53. Denmark Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 54. Norway Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 55. Norway Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 56. Norway Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 57. Norway Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 58. Sweden Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 59. Sweden Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 60. Sweden Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 61. Sweden Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 62. Asia Pacific Cell Culture Media Market, by Country, 2018 – 2030 (USD Million)

Table 63. Asia Pacific Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 64. Asia Pacific Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 65. Asia Pacific Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 66. Asia Pacific Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 67. China Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 68. China Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 69. China Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 70. China Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 71. Japan Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 72. Japan Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 73. Japan Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 74. Japan Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 75. India Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 76. India Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 77. India Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 78. India Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 79. South Korea Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 80. South Korea Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 81. South Korea Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 82. South Korea Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 83. Australia Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 84. Australia Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 85. Australia Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 86. Australia Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 87. Thailand Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 88. Thailand Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 89. Thailand Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 90. Thailand Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 91. Latin America Cell Culture Media Market, by Country, 2018 – 2030 (USD Million)

Table 92. Latin America Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 93. Latin America Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 94. Latin America Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 95. Latin America Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 96. Brazil Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 97. Brazil Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 98. Brazil Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 99. Brazil Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 100. Argentina Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 101. Argentina Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 102. Argentina Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 103. Argentina Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 104. Middle East and Africa Cell Culture Media Market, by Country, 2018 – 2030 (USD Million)

Table 105. Middle East and Africa Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 106. Middle East and Africa Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 107. Middle East and Africa Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 108. Middle East and Africa Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 109. South Africa Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 110. South Africa Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 111. South Africa Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 112. South Africa Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 113. Saudi Arabia Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 114. Saudi Arabia Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 115. Saudi Arabia Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 116. Saudi Arabia Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 117. UAE Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 118. UAE Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 119. UAE Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 120. UAE Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)

Table 121. Kuwait Cell Culture Media Market, by Product, 2018 – 2030 (USD Million)

Table 122. Kuwait Cell Culture Media Market, by Type, 2018 – 2030 (USD Million)

Table 123. Kuwait Cell Culture Media Market, by Application, 2018 – 2030 (USD Million)

Table 124. Kuwait Cell Culture Media Market, by End-use, 2018 – 2030 (USD Million)